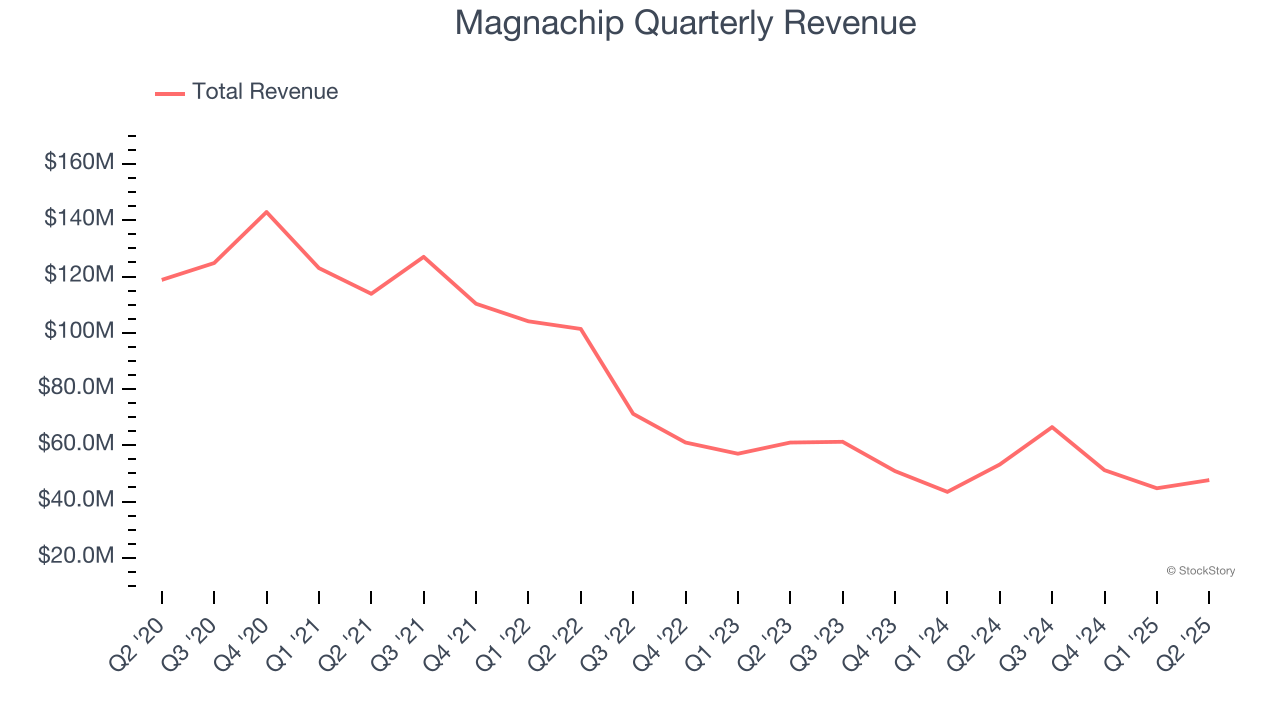

Semiconductor manufacturer Magnachip Semiconductor (NYSE:MX) announced better-than-expected revenue in Q2 CY2025, but sales fell by 10.4% year on year to $47.62 million. On the other hand, next quarter’s revenue guidance of $46 million was less impressive, coming in 15.1% below analysts’ estimates. Its non-GAAP loss of $0.08 per share was 36% above analysts’ consensus estimates.

Is now the time to buy Magnachip? Find out by accessing our full research report, it’s free.

Magnachip (MX) Q2 CY2025 Highlights:

- Revenue: $47.62 million vs analyst estimates of $47.21 million (10.4% year-on-year decline, 0.9% beat)

- Adjusted EPS: -$0.08 vs analyst estimates of -$0.13 (36% beat)

- Adjusted EBITDA: -$2.09 million vs analyst estimates of -$1.3 million (-4.4% margin, relatively in line)

- Revenue Guidance for Q3 CY2025 is $46 million at the midpoint, below analyst estimates of $54.21 million

- Revenue Guidance for CY2025 lowered: "now expected to be flattish as compared to our previous forecast of mid-to-high single digit growth year-over-year, due to a challenging macroeconomic environment related to tariff uncertainty and pricing pressure on older generation products in China"

- Operating Margin: -15.6%, up from -24.1% in the same quarter last year

- Free Cash Flow was -$37.01 million compared to -$2.01 million in the same quarter last year

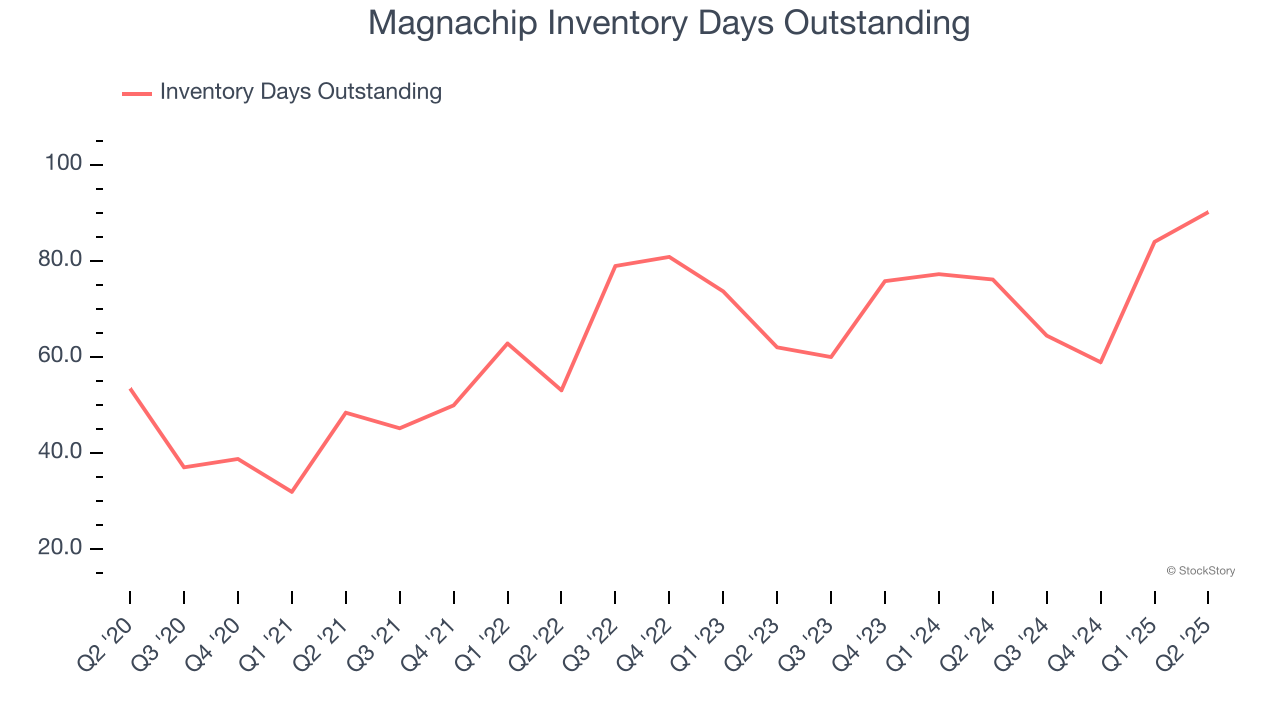

- Inventory Days Outstanding: 90, up from 84 in the previous quarter

- Market Capitalization: $153.6 million

Y.J. Kim, Magnachip’s CEO said, “In Q2, Magnachip delivered our fifth consecutive quarter of year-over-year revenue growth from continuing operations, driven primarily by strong performances in our communications and computing applications businesses. The quarter also benefited from some pull-in activity by customers, which contributed to the overall strength of the results. In industrial applications, we continued to see solid demand across key end markets, including e-motors, LED lighting, and 5G battery management systems.”

Company Overview

With its technology found in common consumer electronics such as TVs and smartphones, Magnachip Semiconductor (NYSE:MX) is a provider of analog and mixed-signal semiconductors.

Revenue Growth

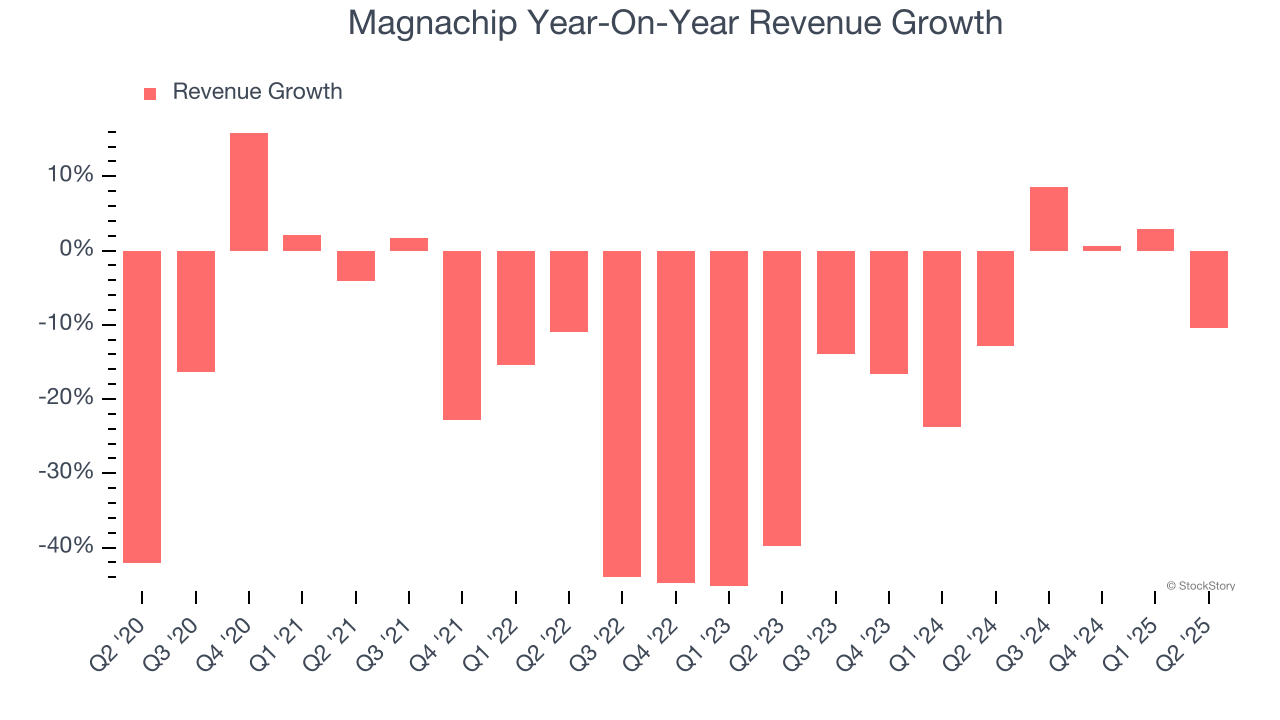

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Magnachip’s demand was weak and its revenue declined by 16.3% per year. This was below our standards and suggests it’s a low quality business. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Magnachip’s annualized revenue declines of 8.4% over the last two years suggest its demand continued shrinking.

This quarter, Magnachip’s revenue fell by 10.4% year on year to $47.62 million but beat Wall Street’s estimates by 0.9%. Company management is currently guiding for a 30.8% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 2.2% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Magnachip’s DIO came in at 90, which is 28 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Magnachip’s Q2 Results

We liked seeing revenue and EPS beat in the quarter. On the other hand, its revenue guidance for next quarter missed and its inventory levels increased. The company also lowered full-year revenue guidance from mid-to-high single digit growth year-over-year to no growth due to "a challenging macroeconomic environment related to tariff uncertainty and pricing pressure on older generation products in China". Overall, this was a softer quarter. The stock traded down 11.6% to $3.65 immediately following the results.

Big picture, is Magnachip a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.