BGC has had an impressive run over the past six months as its shares have beaten the S&P 500 by 16.3%. The stock now trades at $10.79, marking a 24.7% gain. This performance may have investors wondering how to approach the situation.

Following the strength, is BGC a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Are We Positive on BGC?

Tracing its roots back to 1945 and named after founder Bernard Gerald Cantor, BGC Group (NASDAQ:BGC) operates a global brokerage and financial technology platform that facilitates trading across fixed income, foreign exchange, equities, energy, and commodities markets.

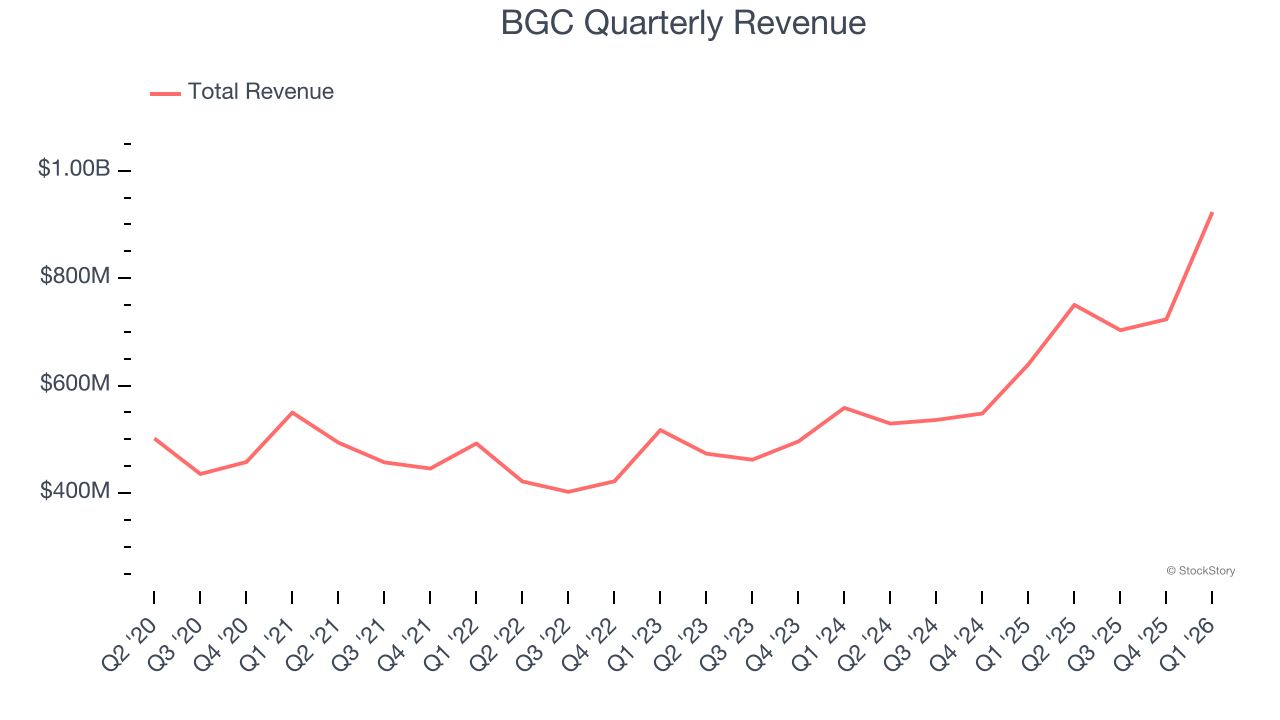

1. Long-Term Revenue Growth Shows Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

Thankfully, BGC’s 9.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

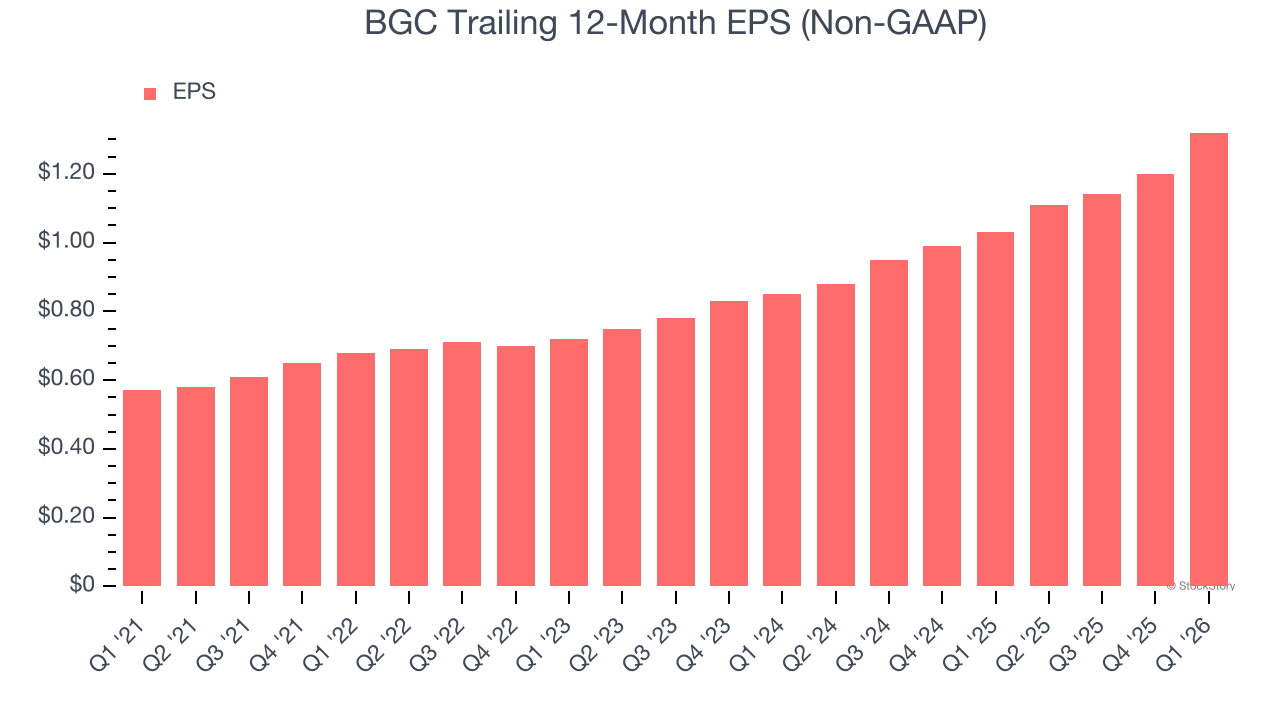

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

BGC’s EPS grew at 18.3% compounded annual growth rate over the last five years, higher than its 9.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

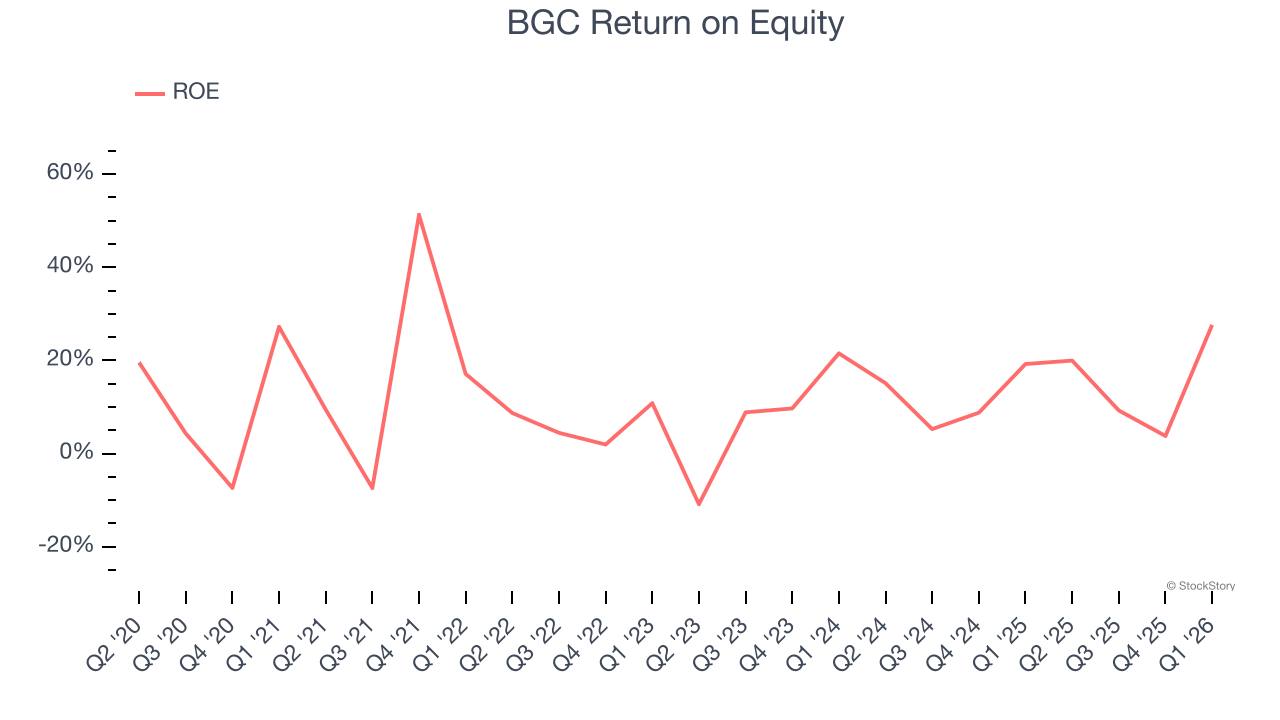

3. Previous Growth Initiatives Are Paying Off

Return on equity (ROE) measures how effectively financial firms generate profit from each dollar of shareholder equity — a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, BGC has averaged an ROE of 11.7%, respectable for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows BGC has a narrow competitive moat.

Final Judgment

These are just a few reasons why we’re bullish on BGC, and with its shares beating the market recently, the stock trades at 7.8× forward P/E (or $10.79 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.